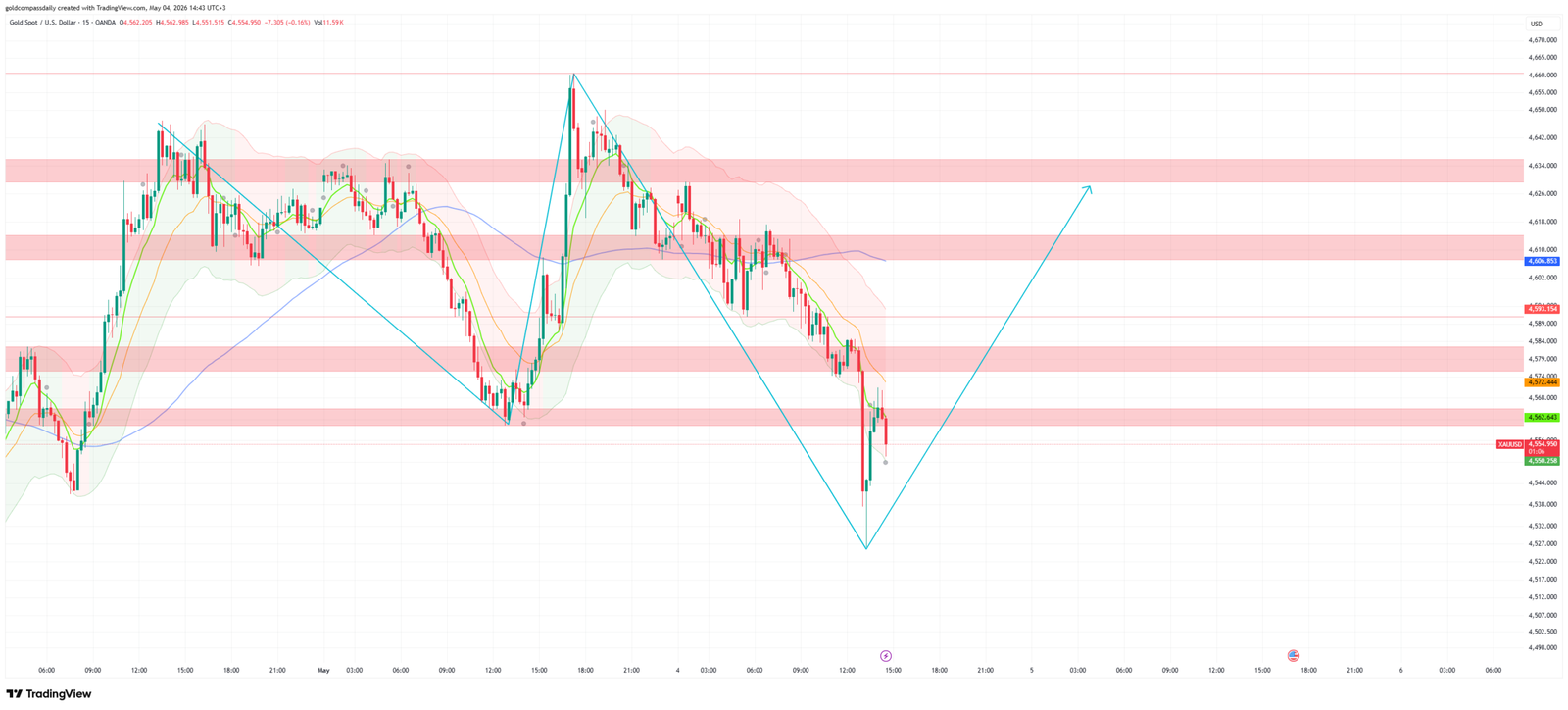

Gold is looking for a floor to open May. After closing April at $4,629 and briefly touching $4,660 at the start of the new month, XAU/USD sold off sharply to $4,525 — driven by a stronger-than-expected US Non-Farm Payrolls report on Friday that reignited dollar strength and forced a reassessment of the Fed cut timeline. Price has since stabilised at $4,554, and the 15-minute chart projects one more dip to $4,525 before a recovery toward $4,634+. Today’s calendar is thin — Japan and the UK are on bank holiday — but the data already published this morning is delivering a string of positive surprises that provide a constructive backdrop for gold’s recovery attempt.

The Chart: NFP Shock Absorbed, Dip Then Recovery

The 15-minute chart shows the aftermath of Friday’s NFP-driven selloff. The sharp drop from $4,660 to $4,525 has created a series of lower highs and lower lows — but the pace of decline has slowed significantly. Price is currently consolidating around $4,554, with the projected path showing one final push into the $4,525 area before buyers absorb the remaining selling pressure and the recovery begins.

The pink resistance bands on the chart — at $4,579, $4,606, $4,610, and $4,634 — are the sequential targets on the recovery path. Each needs to be cleared in turn before the broader April recovery can resume. The immediate resistance is $4,572.441 — a close above that level signals the low is in and the bounce toward $4,606 is underway.

The floor is $4,525. A close below that level opens the $4,488–$4,500 area — the lower green demand zone visible on the chart. Above $4,572, the recovery structure is intact and the target of $4,634+ becomes the session objective.

Friday’s NFP: The Catalyst for the Selloff

Friday’s Non-Farm Payrolls delivered a number that markets did not expect: a strong labour market print that pushed back against the narrative of a weakening US economy building under tariff pressure. The dollar strengthened immediately, real yields moved higher, and gold — which had been positioned for a soft NFP given the deteriorating consumer confidence and weak PMI data — sold off sharply from $4,660 to $4,525.

The critical question is whether the NFP strength reflects genuine economic resilience or is a lagged indicator that hasn’t yet captured the Liberation Day tariff impact. Labour market data typically lags economic conditions by 2–3 months — meaning the April NFP was largely collected before the full tariff shock was felt by businesses. The May and June NFP reports will be the first clean reads on whether Liberation Day is actually affecting US employment. Until then, the strong April NFP creates tension between the labour market signal (resilient) and the forward-looking indicators (deteriorating).

For gold, the NFP selloff from $4,660 to $4,525 is a buying opportunity rather than a structural breakdown — as long as the $4,525 support holds. The fundamental drivers of gold’s 2026 bull case — tariff inflation, global growth uncertainty, safe-haven demand, and eventual Fed easing — have not changed because of one strong payrolls number.

Already Published: Manufacturing PMIs Beat Across the Board

The morning’s PMI data has been uniformly positive — a meaningful contrast to last week’s services PMI disappointments.

Spanish Manufacturing PMI at 51.7 (forecast 49.5, prior 48.7) — a dramatic beat. Spain’s manufacturing sector jumping from 48.7 (contraction) to 51.7 (expansion) in a single month is one of the most significant PMI surprises of the year. The country that was struggling with manufacturing contraction has apparently turned a corner — potentially reflecting pre-tariff order front-running or a genuine recovery in export demand.

Swiss Manufacturing PMI at 54.5 (forecast 52.0, prior 53.3) — a beat. Switzerland’s factory sector expanding at 54.5 confirms last month’s strong reading was not an anomaly. The SNB’s tolerance of franc strength has not crushed Swiss manufacturing — a resilient signal for a small open economy.

Italian Manufacturing PMI at 52.1 (forecast 51.6, prior 51.3) — a beat. Italy’s manufacturing sector accelerating to 52.1 adds to the picture of Southern European manufacturing outperforming expectations.

French Final Manufacturing PMI confirmed at 52.8 (forecast 52.8, prior 52.8) — in line. France’s manufacturing sector in expansion at 52.8 — a significant improvement from the sub-50 readings that characterised most of 2025.

German Final Manufacturing PMI at 51.4 (forecast 51.2, prior 51.2) — a slight beat. Germany’s manufacturing sector holding above 50 for the second consecutive month — the first back-to-back expansion readings since early 2024. This is a meaningful turning point for Europe’s largest economy.

Eurozone Final Manufacturing PMI at 52.2 (forecast 52.2, prior 52.2) — confirmed in expansion. The bloc’s manufacturing sector is growing for the second consecutive month.

The overall European manufacturing picture is the most constructive since before the 2025 slowdown. The key caveat: all of these readings largely predate the full implementation of Liberation Day tariffs. The May readings — due in four weeks — will be the first to fully capture the tariff impact on European factory orders and output.

EUR/USD impact: Manufacturing PMI beats across Europe are EUR-positive — they reduce the urgency of ECB easing and signal that the Eurozone economy entered Q2 with momentum. However, Japan and the UK being on bank holiday today limits liquidity and amplifies the EUR/USD moves. The pair benefits from the positive PMI sweep but faces resistance from the dollar strength generated by Friday’s NFP.

11:30am — Sentix Investor Confidence: The Liberation Day Verdict

The Sentix Investor Confidence printed at -16.4 — better than the forecast of -20.9 and better than the prior -19.2. This is a meaningful beat on a deeply negative index. European institutional investors are less pessimistic about the economic outlook than last month — and significantly less pessimistic than the market expected. A reading of -16.4 versus a forecast of -20.9 is a 4.5-point beat on an index where a 2-point move is considered significant.

The Sentix beat is particularly notable because this survey was conducted after Liberation Day — meaning it captures investors’ actual assessment of the tariff impact rather than anticipation of it. The less-negative reading suggests that European investors are either viewing the Liberation Day tariffs as negotiable/temporary or believe the Eurozone has sufficient buffers to absorb the shock.

EUR/USD impact: Sentix beat is EUR-positive. Combined with the manufacturing PMI sweep, the European session is providing consistent positive surprises that support the euro against a dollar that is strong but vulnerable to any softening in US data this week.

Gold: A Sentix beat that reduces risk-off safe-haven demand is mildly gold-negative in the very short term. However, at -16.4 the index remains deeply in pessimistic territory — investors are less negative, not positive. The structural gold case from European uncertainty remains intact.

All Day — Eurogroup Meetings: Trade Policy Watch

Eurozone finance ministers are meeting today. The primary agenda item is the EU’s coordinated response to US Liberation Day tariffs — including potential retaliatory measures, trade negotiation frameworks, and fiscal coordination. Any announcement of significant EU retaliatory tariffs would be a risk-off event that supports gold. Any announcement of negotiation progress or tariff exemptions would be risk-on and mildly gold-negative. This is the most underappreciated event risk of today’s session — watch for headlines throughout the day.

5:00pm — US Factory Orders: The First May US Data Point

US Factory Orders m/m is forecast at 0.5% (prior 0.0%). A reading of 0.5% would signal that US manufacturers placed meaningfully more new orders in March — a positive economic signal that would add to Friday’s NFP in building the case that the US economy was resilient heading into Liberation Day. A miss below 0.2% would raise questions about business confidence and investment intentions ahead of the tariff implementation.

This is the first significant US economic data of May and will set the initial tone for how markets interpret the strength of the US economy post-Liberation Day. Given the dollar’s strength from Friday’s NFP, a weak Factory Orders print would be the most direct near-term catalyst for a dollar pullback and gold recovery toward $4,572.

7:50pm — FOMC Member Williams: Post-FOMC Communication

FOMC Member Williams speaks at 7:50pm — the New York Fed President and one of the most influential voices on the committee. This is the first scheduled Fed communication since Wednesday’s balanced FOMC hold, and Williams will have the benefit of seeing Friday’s strong NFP data alongside the deteriorating forward-looking indicators. His framing of the tension between a resilient labour market and softening growth expectations will be the most important Fed signal of the week ahead of Thursday’s claims data.

Any language suggesting that the strong NFP does not change the Fed’s assessment of “two-sided risks” would be dollar-negative and gold-positive — confirming that the balanced FOMC tone from Wednesday is the sustained message rather than a one-time acknowledgement. A more hawkish Williams — emphasising that the NFP strength justifies maintaining the current rate path — would add to the dollar’s NFP-driven gains and extend gold’s pressure toward $4,525.

10:30pm — BOC Governor Macklem: Canadian Perspective

BOC Governor Macklem speaks at 10:30pm. Canada is on the front line of Liberation Day tariff exposure — automotive, energy, and agricultural exports to the US have all been directly affected. Macklem’s assessment of the Canadian economic outlook and the BOC’s policy response will be closely watched for signals about the pace of further cuts. Any dovish language from Macklem would be CAD-negative and could spill over into broader risk sentiment for overnight markets.

Key Levels and Full Market Summary

- Gold (XAU/USD): $4,554 · Dip target $4,525 · Resistance $4,572 → $4,579 → $4,606 → $4,634 · Target $4,634+ · Floor $4,500 · Factory Orders 5:00pm + Williams 7:50pm are the catalysts

- EUR/USD: Manufacturing PMI sweep + Sentix beat = positive European session · Dollar strength from NFP is the headwind · Factory Orders 5:00pm shapes afternoon · Williams 7:50pm drives the close

- GBP/USD: UK bank holiday — sterling absent · Pair moves with USD direction from US data · Reopens Tuesday with full UK liquidity

- USD/JPY: Japan bank holiday — yen liquidity thin · NFP-driven dollar strength = pair elevated · Williams 7:50pm is the key directional input · Dovish Williams = sharp pair decline when yen liquidity returns Tuesday

- AUD/USD: ANZ Job Advertisements at -0.8% (prior -3.2%) = improvement in Australian employment outlook · Building Approvals collapse -10.5% = housing sector stress · Net: mildly negative · Moves with risk sentiment from Eurogroup and Williams

- S&P 500 / Nasdaq: NFP strength positive for growth narrative · Manufacturing PMI beats = constructive open · Factory Orders at 5:00pm adds US data context · Williams hawkish = equity headwind · Williams balanced = modest rally

- DAX: German manufacturing PMI beat (51.4) + Sentix improvement = constructive European session · Eurogroup tariff response is the key risk event · Positive surprise from Eurogroup negotiations = DAX rally

- EUR/GBP: UK absent today — cross illiquid · Full EUR/GBP price discovery resumes Tuesday

- WTI Crude: Thin liquidity (Japan + UK holiday) amplifies moves · Global manufacturing PMI beats = demand-positive · Eurogroup retaliation risk = global trade uncertainty headwind

- Gold structural case: NFP selloff is a buying opportunity · $4,525 is the floor · Manufacturing PMI beats + Sentix improvement = risk-on backdrop · Williams balanced tone = recovery toward $4,634 · Tariff inflation + Fed uncertainty = multi-week bull case intact

May opens with gold under pressure but not broken. The NFP shock created the dip — the manufacturing PMI sweep and Sentix beat are providing the foundation for the recovery. The $4,525 support is the line in the sand. Hold it, and the April recovery narrative continues toward $4,634 and beyond. Lose it, and $4,488–$4,500 becomes the next test. Williams at 7:50pm will tell us which way the Fed is leaning — and that, more than any technical level, determines where gold goes this week.

Analysis based on the XAU/USD 15-minute chart as of May 4, 2026, 14:43 UTC+3. Economic data sourced from the daily macro calendar. This article is for informational and educational purposes only and does not constitute financial advice.