The US stock market is starting the first full week of February 2026 on the back foot, as a wave of uncertainty sweeps across Wall Street. This Market index performance February 2026 report highlights a broad-based decline across major benchmarks, triggered by a combination of political shifts at the Federal Reserve and high-stakes economic data releases. As the opening bell rings, the primary narrative is one of caution, with investors recalibrating their portfolios for a potentially more hawkish monetary environment.

The Indices in Red: S&P 500 and Nasdaq Under Pressure

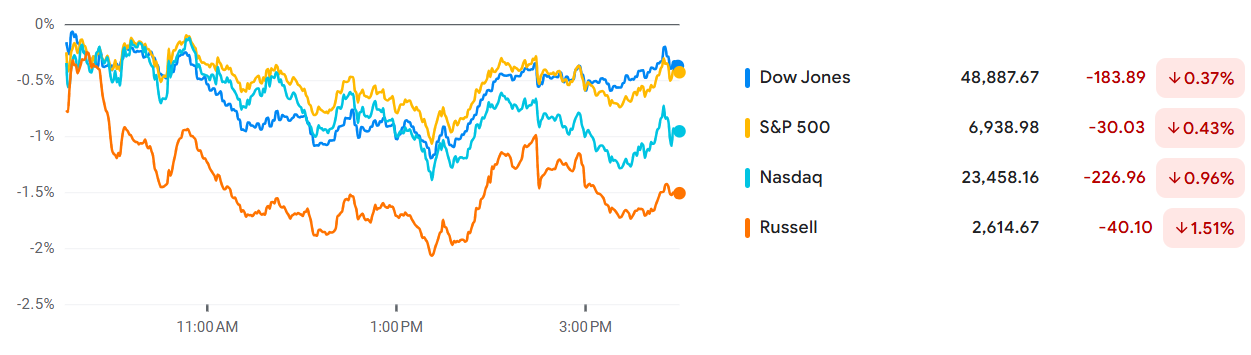

As seen in the latest snapshot, the Market index performance February 2026 shows the S&P 500 (US500) trading lower at 6,897, a decline of 0.43% for the day. This pullback follows a period of record highs, suggesting that the market is entering a necessary consolidation phase. More significantly, the tech-heavy Nasdaq Composite (US100) is leading the retreat, dropping 0.72% to 23,685. The Dow Jones Industrial Average (US30) is also showing weakness, slipping 0.37% to 48,712, as cyclical sectors face renewed scrutiny.

The negative sentiment is further amplified by a spike in the Cboe Volatility Index (VIX), which has surged over 6% to 17.92. This jump in the “fear gauge” indicates that traders are actively hedging against further downside risk. The technical charts for the Nasdaq 100 suggest a potential double-top formation, a bearish signal that could lead to a deeper correction toward the 24,500 support level if current selling pressure persists throughout the session.

[Image: Table of Major Index Performance – S&P 500, Dow Jones, Nasdaq]The Kevin Warsh Nomination: A Hawkish Shift?

The primary fundamental driver behind this Market index performance February 2026 is President Trump’s nomination of Kevin Warsh as the next Chair of the Federal Reserve. Warsh, known for his disciplined and inflation-focused approach during his previous tenure as a Fed Governor, is perceived by the market as a “hawk.” His potential leadership suggests a more cautious path toward interest rate cuts, which has immediately pushed the US Dollar Index (DXY) higher to 96.64.

This “Warsh Shock” has not only pressured equities but has also caused a historic collapse in precious metals, which were hammered as Treasury yields edged upward. For stock investors, higher-for-longer interest rates mean higher borrowing costs and a potential compression of valuation multiples, particularly in the high-growth technology sector. The market is now pricing in a 35% probability of a recession later in 2026, adding another layer of complexity to the current trading environment.

Upcoming PMI Data: The Industrial Health Check

As the session progresses, the Market index performance February 2026 will be heavily influenced by the release of the S&P Global Manufacturing PMI and the ISM Manufacturing PMI reports. Forecasts suggest a reading of 51.9, which would indicate a modest expansion in the industrial sector. However, the market is particularly sensitive to the “Prices Paid” and “Employment” components of these reports.

A stronger-than-expected PMI reading could be a double-edged sword. While it signals economic resilience—a positive for corporate earnings—it also provides the Federal Reserve with more room to maintain a restrictive policy stance. Conversely, a miss in the data could spark fears of a manufacturing slowdown, potentially triggering a move toward safe-haven assets. Traders are currently “wait-and-see,” with liquidity remaining thin ahead of these 10:00 AM ET releases.

Individual Stock Moves and Sector Divergence

Within the Market index performance February 2026, we are seeing significant divergence. Apple shares have slipped 1% despite beating earnings expectations, as investors worry about rising costs and the impact of the stronger dollar on international revenue. Similarly, Exxon Mobil has pulled back 1.5% amid weaker crude prices, even after exceeding profit estimates. On the positive side, Sandisk (SNDK) skyrocketed 23% in pre-market trading following a massive earnings beat driven by the ongoing AI supercycle.

The healthcare sector remains a significant drag on the Dow, with UnitedHealth and Humana continuing to slide following the expiration of Affordable Care Act subsidies. This sectoral rotation suggests that while the “AI trade” is still active, the broader market is becoming increasingly fragmented, requiring a more surgical approach to stock selection than in previous months.

Conclusion: Navigating the February Volatility

In summary, the Market index performance February 2026 for today is defined by a recalibration of risk. The combination of the Warsh nomination and the looming PMI data has created a “sell-the-news” environment after a strong January. Until the S&P 500 can reclaim its pivot zone near 6,975, the near-term outlook remains subdued.

For intraday traders, the strategy should focus on the 25,200 support for the Nasdaq and the 48,400 level for the Dow. Breaking below these marks could open the door for a more consistent outflow as month-end flows settle. Stay tuned for our next update following the ISM release, where we will analyze the real-time reaction of the major indices to the latest economic health check.

As always, keep your stops tight and your eyes on the VIX. The 2026 market cycle is proving to be a year of intense macro-driven shifts.